Does Homeowners Insurance Cover All-natural Calamity Problems? Danger insurance policy might omit particular kinds of damages, such as losses from a flooding or a sinkhole. For homes prone to these threats, purchasing optional added homeowners insurance coverage may be advisable. That's leading some individuals to downsize protection or perhaps do without. As natural disasters remain to influence areas worldwide, it's all-natural to have inquiries concerning exactly how they can affect your insurance coverage. This places the overall cost of billion-dollar catastrophes to greater than $1.1 trillion over the past 10 years. Environment change plays a major function in the regularity and intensity of extreme climate. House owners bear the impact of the monetary worry and require to have ample insurance policy protection or danger paying of pocket to restore their homes. House owners insurance does not cover damages to your auto triggered by natural calamities. A hazard is an insurance policy term for something that presents a threat of loss, while a risk increases the danger of loss. Wildfires are natural dangers since they boost the risk of loss from a fire. Dry spells are the second-biggest all-natural catastrophe that affects the U.S., with Fallon, Nevada experiencing dry spells averaging 184.5 weeks. Dry spells cause the planet below your home to dry out and reduce, which could cause your structure to split.

Typhoon Wind Damages

As an example, an HO-3 consists of open-peril house protection, but it does Commercial Auto Insurance in La Puente, CA have a few major exemptions, that include earthquake, flooding, and overlook. On the various other hand, named-peril policies will only cover the certain risks noted within the policy, as it does not offer as wide insurance coverage DMV registration services in Riverside CA compared to open-peril policies. Sometimes homeowner's insurance can include both open-peril and named-peril sections, as it's important to connect to your insurance policy agent to learn more about these details. In general, coverage for wildfire damages is generally consisted of in home owners' and commercial residential or commercial property insurance plan. These policies normally cover damage caused by wildfires to structures like homes and structures in addition to personal belongings.States Most At Risk for Natural Disasters - ValuePenguin

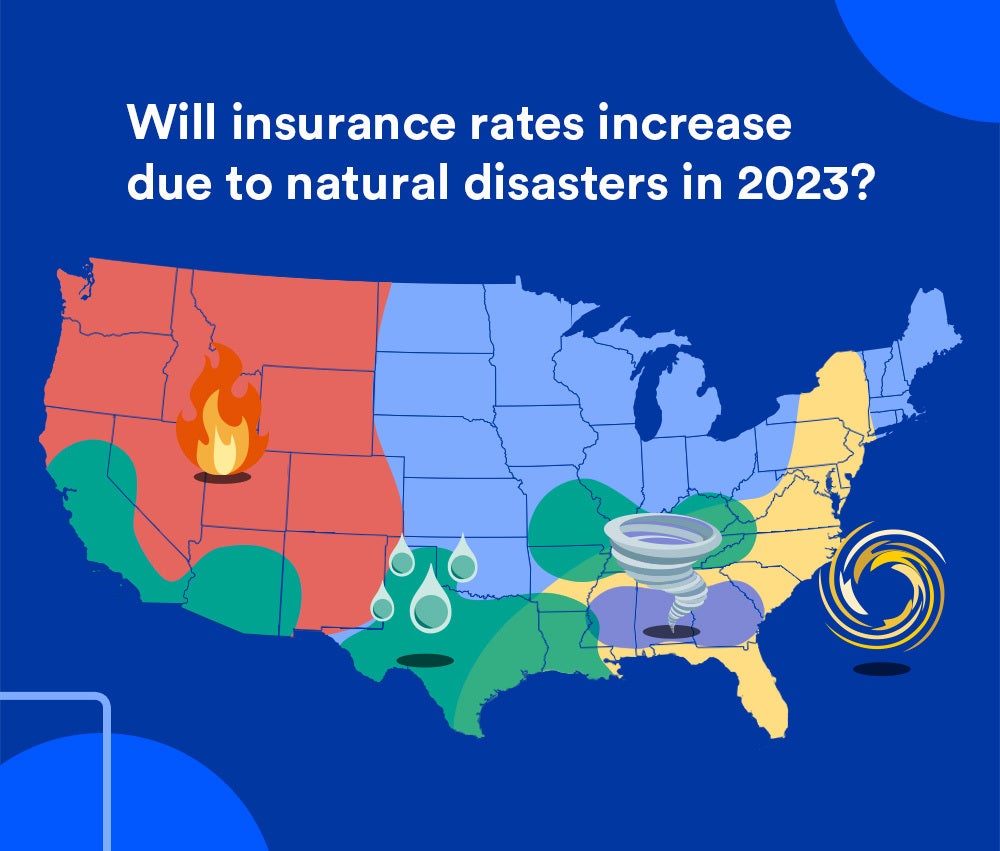

States Most At Risk for Natural Disasters.

:max_bytes(150000):strip_icc()/homeowners-insurance-guide_final-88e7d3469dcc4920977498f08564b234.png)

Posted: Mon, 08 Jun 2020 07:00:00 GMT [source]

Why Homeowners Insurance Coverage Rates Are Climbing

Choosing a higher deductible will usually reduce your home insurance policy costs but you will certainly get less cash if you submit a damages or burglary case. Yet if a tree drops because of an issue covered by your policy and blocks your driveway, your policy could cover debris elimination up to a defined restriction. As an example, a plan may pay up to $1,000 for debris elimination costs. Optional coverages consist of HostAdvantage to cover your items when home-sharing, and flooding insurance coverage with the NFIP. Personal property insurance coverage normally enforces limits on the quantity the home insurer will certainly pay for details kinds of home. For instance, a home owners insurance policy may cover an optimum of $1,500 worth of precious jewelry no matter whether the homeowner had a beneficial gem collection. To deepen your understanding of just how natural catastrophes in 2023 can affect insurance coverage prices, we suggest discovering our collection of relevant articles.- To the most effective of our expertise, all web content is accurate since the day published, though offers consisted of herein may no more be readily available.If you have protection for food putridity, your policy will certainly have a specified restriction, such as $500.Typhoon damages brought on by wind and hailstorm is typically covered, though there may be restricted protection or a separate, higher deductible if you stay in a coastal area.Higher deductibles usually result in lower costs, however it is necessary for property owners to choose an insurance deductible that they can conveniently afford in the event of a flood-related insurance claim.Your input is extremely appreciated and crucial in maintaining the precision of our content.